Deciphering the Process: Just How Can Discharged Bankrupts Obtain Debt Cards?

Browsing the realm of credit history card applications can be an overwhelming task, especially for individuals who have been released from insolvency. The process of restoring credit scores post-bankruptcy presents special obstacles, often leaving several questioning about the expediency of obtaining credit cards as soon as again. Nevertheless, with the appropriate methods and understanding of the qualification requirements, released bankrupts can start a trip towards monetary recuperation and accessibility to credit scores. Yet how precisely can they browse this elaborate procedure and safe and secure bank card that can aid in their credit history rebuilding journey? Allow's discover the avenues offered for discharged bankrupts aiming to reestablish their credit reliability via bank card options.

Recognizing Bank Card Qualification Standard

One crucial consider charge card eligibility post-bankruptcy is the individual's credit rating. Lenders often consider credit rating as a measure of a person's credit reliability. A greater credit rating signals accountable financial behavior and might bring about much better bank card choices. Additionally, showing a secure earnings and employment background can positively influence bank card authorization. Lenders look for guarantee that the individual has the methods to repay any kind of credit history reached them.

Additionally, people ought to know the different kinds of bank card available. Safe charge card, for circumstances, require a money deposit as collateral, making them much more available for people with a history of personal bankruptcy. By comprehending these qualification requirements, individuals can navigate the post-bankruptcy credit rating landscape a lot more properly and work in the direction of reconstructing their monetary standing.

Restoring Credit After Personal Bankruptcy

After insolvency, people can start the procedure of rebuilding their credit history to boost their monetary stability. One of the preliminary action in this procedure is to acquire a guaranteed charge card. Secured bank card call for a cash money deposit as collateral, making them more easily accessible to people with an insolvency background. By utilizing a safeguarded credit rating card responsibly - making timely payments and maintaining equilibriums reduced - people can demonstrate their creditworthiness to potential lenders.

An additional method to restore credit rating after personal bankruptcy is to come to be an authorized user on a person else's bank card (secured credit card singapore). This allows people to piggyback off the primary cardholder's favorable credit rating, potentially enhancing their own credit scores score

Consistently making on-time settlements for debts and expenses is critical in rebuilding credit scores. Settlement history is a considerable variable in identifying credit report, so showing accountable financial behavior is important. In addition, consistently checking credit scores reports for mistakes and inaccuracies can assist make certain that the details being reported is right, more assisting in the credit scores rebuilding process.

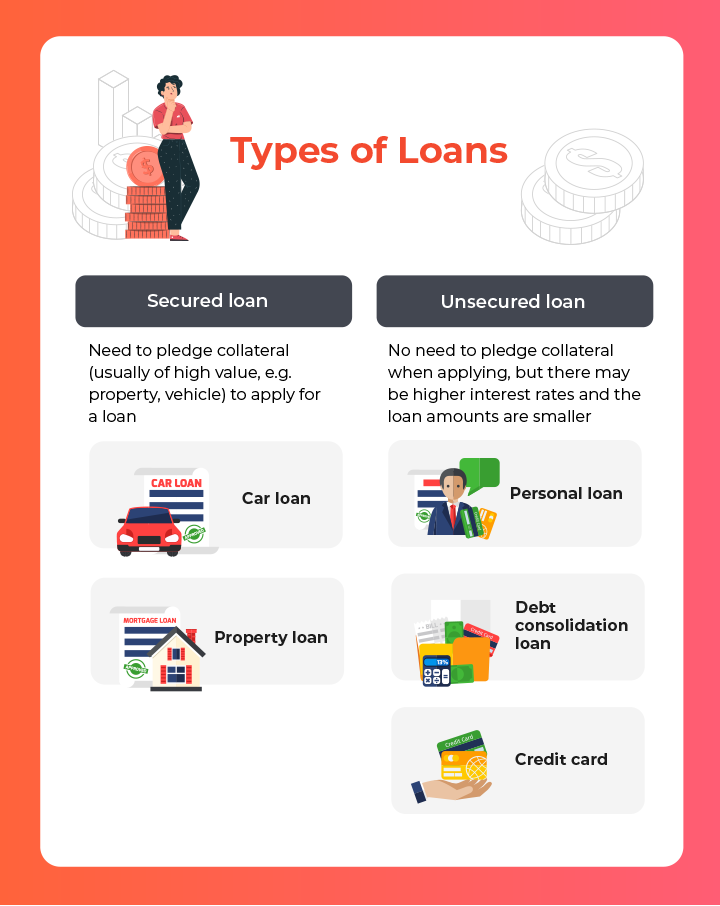

Safe Vs. Unsecured Credit Rating Cards

When thinking about bank card alternatives, people might run into the selection between protected and unprotected charge card. Secured bank card need a money deposit as collateral, usually equal to the credit report limitation approved. This deposit safeguards the company in case the cardholder defaults on payments. Secured cards why not try here are frequently recommended for people with bad or no credit rating, as they give a means to restore or construct debt. On the various other hand, unprotected charge card do not require a down payment and are approved based upon the cardholder's credit reliability. These cards are much more usual and usually included greater credit line and lower fees contrasted to protected cards. Nonetheless, individuals with a background of bankruptcy or bad credit history may discover it testing to receive unsecured cards. Selecting in between safeguarded and unsecured credit rating cards relies on a person's monetary circumstance and credit score goals. While secured cards offer a course to enhancing credit history, unsecured cards give more versatility however might be more difficult to obtain for those with a struggling credit rating.

Making An Application For Credit Cards Post-Bankruptcy

Having reviewed the distinctions between unprotected and secured bank card, people who have actually undertaken bankruptcy may currently think Web Site about the process of making an application for charge card post-bankruptcy. Rebuilding debt after bankruptcy can be difficult, however getting a bank card is a critical step towards boosting one's creditworthiness. When requesting charge card post-bankruptcy, it is important to be selective and calculated in selecting the appropriate options.

Additionally, some individuals might certify for certain unsafe credit report cards especially developed for those with a history of insolvency. These cards might have higher fees or rate of interest rates, yet they can still offer a chance to restore credit history when made use of sensibly. Prior to getting any bank card post-bankruptcy, it is a good idea to assess the conditions carefully to understand the fees, rates of interest, and credit-building potential.

Credit-Boosting Techniques for Bankrupts

Reconstructing credit reliability post-bankruptcy requires carrying out efficient credit-boosting approaches. For people aiming to boost their credit rating after personal bankruptcy, one crucial method is to acquire a protected charge card. Protected cards require a cash money down payment that serves as collateral, making it possible for people to demonstrate responsible credit rating use and repayment behavior. By making timely settlements and maintaining credit rating utilization reduced, these individuals can progressively reconstruct their creditworthiness.

An additional method involves ending up being an authorized individual on someone else's bank card account. This enables people to piggyback off the primary account owner's favorable credit report, potentially enhancing their own credit history. Nonetheless, it is crucial to make sure that the key account owner maintains great credit practices to make the most of the advantages of this approach.

In addition, regularly keeping an eye on credit rating reports for mistakes and contesting any kind of mistakes can also help in enhancing credit rating. By remaining aggressive and disciplined in their credit scores monitoring, people can progressively boost their credit reliability also after experiencing personal bankruptcy.

Final Thought

In verdict, released bankrupts can get bank card by meeting eligibility criteria, restoring credit scores, understanding the difference in between safeguarded and unsafe cards, and using tactically. By following credit-boosting strategies, such as maintaining and making prompt payments debt application reduced, bankrupt individuals can progressively improve their credit reliability and accessibility to credit cards. It is necessary for released bankrupts to be thorough and mindful in their financial actions to efficiently navigate the procedure of acquiring credit score cards after personal bankruptcy.

Comprehending the stringent credit card qualification criteria is essential for people seeking to get credit score cards after insolvency. While protected cards offer a course to enhancing debt, unprotected cards provide even more flexibility however might be harder to get for those with a troubled credit scores background.

In verdict, discharged bankrupts can get credit history cards by fulfilling eligibility requirements, restoring credit history, recognizing the difference in between protected and unsafe cards, and applying tactically.